Tax Optimisation Tool-Hindu Undivided Family

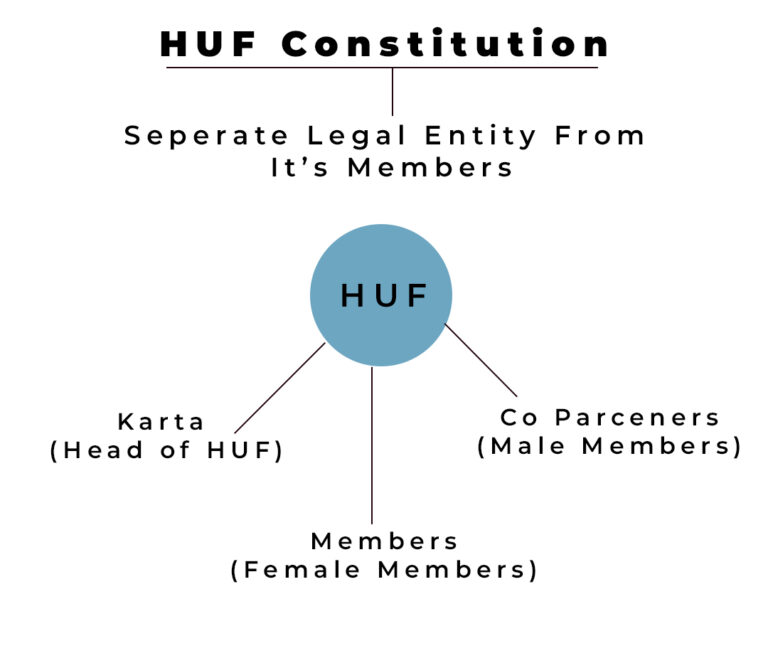

A Hindu Undivided Family (HUF) is made up of Karta , coparceners and members under Indian succession rules.

Popular Articles

.png)

CONTACT US

ADDRESS

10 ,Basement, Vinoba Puri, Lajpat Nagar II, New Delhi, Delhi 110024

Call

Email ID